A common adage in economics is “there is no such thing as a free lunch”. Although generally true, exceptions do exist. One such exception relates to a Social Security loophole that the Bipartisan Budget Act of 2015 closed for those born January 2, 1954, or later¹. This loophole remains open for those born January 1, 1954, or earlier. Since this applies to a declining subset of the population, this loophole is receiving progressively less media and consultant attention.

"Free lunch" From Social Security Benefits Loophole

Tim Sittler, CAIA, CFP®

This loophole allows an individual to start collecting spousal benefits from Social Security while their personal benefit continues to earn delayed retirement credits for as much as a 32% increase over their full retirement age (FRA) benefit amount. In other words, they are able to start receiving a spousal benefit from Social Security without any consequence to their personal benefit. This is accomplished by filing a “restricted application for spousal benefits only” with Social Security and then switching to your personal benefit at age 70.

In order to take advantage of this loophole, it is important to understand the basic requirements. First, to collect spousal benefits while married², your spouse must be collecting their retirement benefit. Second, you must be born before January 2, 1954 and file the restricted application at or beyond your FRA. Lastly, you cannot be collecting your personal benefit. If you meet these criteria but have already passed your FRA, you could still receive some benefit from the strategy by filing the restricted application prior to reaching age 70 and requesting up to six months retroactive spousal benefits, assuming your spouse was receiving benefits for at least six months or has also filed to retroactively receive benefits going back six months.

When pursuing this strategy, be prepared for some confusion or even pushback as not all Social Security representatives will be well versed in this area and may think the new “deemed filing” rules apply to everyone. If you believe you are eligible and are being told otherwise, usually asking for a supervisor will resolve any confusion. Additionally, you can reference the information from the first footnote of this article from the Social Security website.

Adding up the benefits

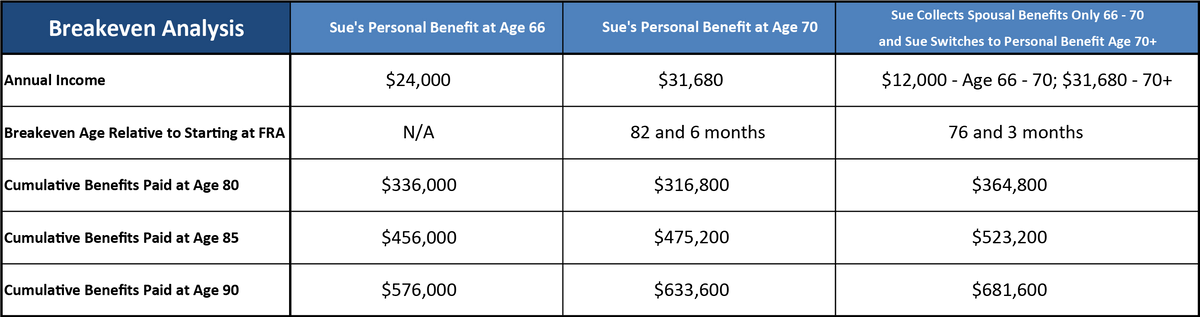

As an example, consider Fred and Sue Smith. For the purposes of an easy illustration, do not consider cost of living adjustments, and assume both will be eligible to receive a monthly benefit of $2,000 at their full retirement age 66. Fred turns 66 first and elects to begin taking his benefit. A few months later, Sue turns 66 and rather than starting her benefit of $2,000/month, she elects to file a “restricted application for spousal benefits only” and begin collecting $1,000/month based on Fred’s work history. They are now receiving $3,000/month collectively, while Sue’s personal retirement benefit continues to grow each month she delays taking it. At age 70, Sue’s personal benefit has now reached its maximum level and she switches from her spousal benefit to her maximized personal benefit of $2,640/month. This is a significant, permanent increase in monthly benefits. Moving forward, rather than receiving $24,000/year as she would have with her FRA benefit of $2,000/month, she’ll receive $31,680/year for the rest of her life. Additionally, should Fred survive Sue, he would be entitled to this higher benefit for the rest of his life as a survivor’s benefit since it is greater than his personal benefit.

By taking advantage of this loophole, the age at which Sue reaches a breakeven on cumulative benefits from Social Security by waiting to age 70 versus starting her benefit at FRA is greatly reduced. If she receives no benefits from age 66 to age 70 and then starts with her maximized benefit of $2,640/month, she would have to collect benefits until age 82.5 to reach the same cumulative benefits paid from her lower FRA benefit of $2,000/month starting at age 66³. By receiving a spousal benefit of $1,000/month from 66 to 70, the breakeven drops to age 76 and 3 months in this example⁴. In all instances this strategy will reduce the breakeven age, but the degree of the reduction will depend on the amount of the spousal benefit relative to the individual’s personal benefit and whether or not they can claim a spousal benefit for the full deferral period from age 66 to age 70.

¹ https://www.ssa.gov/planners/retire/deemedfaq.html

² If you were married more than 10 years, did not remarry before age 60, and have been divorced at least 2 years you are considered “independently entitled” to Social Security benefits and can actually file for full spousal benefits whether your ex-spouse has filed or not as long as you’ve both reached full retirement age.

³ 198 months from age 66 at $2,000/mo. = $396,000. 150 months from age 70 at $2,640/mo. = $396,000. Breakeven age of 82 and 6 months can be found by adding number of months to both starting ages.

⁴ 123 months from age 66 at $2,000/mo. = $246,000. 48 months from age 66 to age 70 at spousal benefit of $1,000/mo. + 75 months from age 70 at maximized benefit of $2,460/mo. = $246,000. Breakeven age of 76 and 3 months can be found by adding number of months to both starting ages.

Securities offered through Calton & Associates, Inc. member FINRA/SIPC. OSJ 2701 N. Rocky Point Dr., Suite 1000, Tampa, FL 33607 (813) 605-0918 Advisory services offered through Waterloo Capital, L.P. an SEC Registered Investment Adviser. Calton & Associates, Inc. and Waterloo Capital, L.P. are separate entities.